Looking back at the 75th Anniversary of the D-Day landing a few months ago, it reminded me of the huge changes that have happened to Lancaster and more specifically the Lancaster property market since WW2. Back in 1946, the average wage in Lancaster was just over £5 a week and to buy an average car would cost you just under £600, yet this is a property blog, so…

The average value of a Lancaster property in 1946 was £887

In fact, in those 75 years, the average Lancaster house had doubled in price by 1961, then again in 1971, 1975, 1980, 1988, 2000 and 2006. Now a lot of those increases (especially in the 1970’s) were caused by hyperinflation, yet since the start of the 21st Century inflation has been kept low and since the Credit Crunch (2008/9), whilst property values have been rising, they haven’t been at the rates experienced in the latter half of the 20th Century.

Now what a property sells for is irrelevant. The important thing is whether someone can afford it.

Increases in Lancaster property values have produced huge increases in equity for many Lancaster homeowners and Lancaster buy to let landlords, yet on the other side of the coin this is also making housing unaffordable for other people. The best measure of the affordability of housing is the ratio of Lancaster property values to Lancaster average earnings (i.e. salary/wages). This ratio works on the basis the higher the ratio, the less affordable properties are.

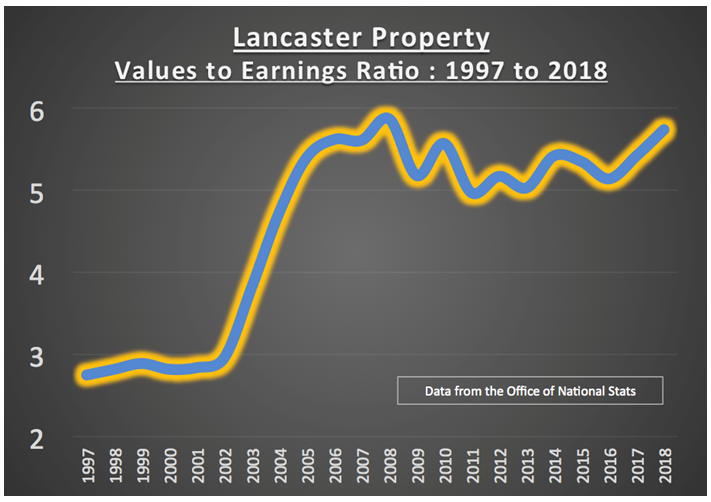

In 1997, the average value of a Lancaster property was 2.8 times higher than the average annual wage in Lancaster, in 2008 it peaked at 5.9, yet one year later it had dropped to 5.2 and since then has slowly risen back to 5.7 times higher!

It can be seen that even though property in Lancaster became more affordable after the 2007/8 property crash (i.e. the ratio dropped), in recent years, with house values rising but earnings/salaries not keeping up, the ratio started to rise. This has meant there has been a decline in affordability of property in Lancaster over the last five years – so for those on particularly low incomes or with little capital, it unfortunately means that buying a Lancaster home will never become an option.

Therefore, the demand for private rented properties in Lancaster will continue to grow as many young people are deciding to rent instead of buy their own house (knowing when their parents pass away, the equity built up in their parents property will be passed down – and then they can buy in their 50’s and 60’s – just like it happens in Germany).

Yet, that is many decades away and with fewer Lancaster people wanting or able to save up the 5% deposit required by mortgage lenders, more and more people are looking to rent. Tie this in with the subtle shift in attitudes towards renting since the Millennium and fewer people jumping on the bottom rung of the property ladder, this has driven rents and demand up in Lancaster over the last few years. Yet (and it’s an important proviso) the type, location and demands of Lancaster tenants has changed over that same time frame, meaning you can’t just make money from buy to let as easily as falling off a log like you did in the early 2000’s.

If you are an existing landlord with us (or even another agent in Lancaster) or you’re thinking of becoming a first time Lancaster landlord, looking for advice and opinion and what (or not to buy in Lancaster), one source of information is the Lancaster Property Blog – or drop me an email or phone call and let’s start a conversation – I don’t bite and I don’t do hard sell … and maybe, just maybe, I could help you get better returns from your property portfolio.